TSLA (EASYMARKETS: TSLUSD)

On October 18th, Tesla Inc. reported its earnings for Q3, which came out as a disappointment. The EPS fell by 0.07 USD to 0.66 USD, as the estimate sat near 0.73 USD. The decline equated to around 9.48%. Revenue also declined, as it missed its initial forecast by around 837 million USD. This report marked the first time since April 2021 that Tesla reported a miss on earnings. For obvious reasons, the stock took a beating the same day. It continued its journey south a couple of trading sessions afterwards. But after finding strong support near the 200-dollar mark, the stock rebounded and is now trying to make its way towards its short-term downside resistance line drawn from the high of July 19th. A break of that trendline could invite more buyers into the game, possibly clearing the way towards the current highest point of this year, near the 300-dollar mark.

Recently, some analysts lowered their price targets for TSLA to a median of around 260 USD per share because Tesla Inc. might struggle with its growth in the near term. And there are grounds for that as the company decided to hold off from expanding in Mexico with their initial plan to establish a factory there.

Another headwind is the current fall in demand for electric vehicles. We believe that consumers have become even more educated on not only the benefits of electric vehicles but also on the negative aspects of EV maintenance and after-life battery utilization. The process of utilization of old batteries could be more eco-friendly. Also, as we know, EV batteries consist of metals like Nickel, Lithium, Cobalt, Aluminum, and others. It is no secret that some of these crucial elements are found in countries where political unrest is a common occurrence, or the country might be under sanctions. Also, it is generally understood by many that in some countries, the mining of these metals is performed by minors. This state of origin puts the use of these raw materials under question, throwing a shadow on the whole industry.

Interest rates are another problem that car manufacturers are facing. Rising interest rates are becoming an obstacle in making the end product affordable to the consumer. Not only do rising rates make borrowing costs higher for the companies, but they also make it more expensive for people to lease the desired vehicles. However, this doesn’t only concern the EV market. This increasing expense is an issue across developed and emerging economies.

Now, another little issue, which had recently come up on the Tesla side, is the manufacturing of the long-awaited Cybertruck. Elon Musk himself had described the truck as a problematic one because of the vehicle’s unique design and the sophisticated technology behind it. According to the recent comments from Mr. Musk, it will take some time before the company becomes cash flow positive on the Cybertruck.

PG (EASYMARKETS: PNGUSD)

On the same day Tesla Inc. reported its earnings, Procter & Gamble Co. shared its Q3 earnings with the world. The company showed good results, with EPS coming out at 1.83 USD, which is better than the estimated 1.72 USD. This is approximately a 6.4% increase. Revenue was also slightly higher, beating the initial forecast by 1.35%. During the next few trading sessions after the earnings release, the stock drifted lower. That said, judging from the technical analysis side, this could be classed as a temporary correction before another possible leg of buying. However, other important aspects need to be considered about the company first.

The company falls into the consumer non-durables (or consumer staples) category in the household/personal care industry. It operates mainly in the following five segments: Beauty, Grooming, Health Care, Fabric & Home Care, and Baby, Feminine & Family Care. The company sells its products in approximately 180 countries and territories primarily through mass merchandisers, grocery stores, membership club stores, drug stores, department stores, distributors, baby stores, specialty beauty stores, e-commerce, high-frequency stores, and pharmacies. PG offers products under brands such as Olay, Old Spice, Safeguard, Head & Shoulders, Pantene, Rejoice, Mach3, Venus, Cascade, Dawn, Febreze, Mr. Clean and others.

Consumer staples stocks tend to perform well during economic downturns because those companies sell products that are still used by people during harsh economic times and are difficult to substitute or remove because of their necessity. So, given that market participants expect at least some economic downturn in the near term, such cash-rich publicly traded companies as Procter & Gamble Co. fall into the spotlight. This makes their stocks more attractive to potential investors, who not only try to speculate on the possibility of a future price increase but also as a way of safeguarding a portion of their investments. P&G is also one of those companies that currently pays a yearly dividend of around +2.43% on just holding the stock.

One of the threats for such companies is to rely purely on price increases. Although the products and their quality can be modernized and upgraded, this doesn’t happen very quickly, hence the dependence on the price for which the product is sold becomes very high. The price increase is seen as a good strategy in the short term, but this is not very viable in the long term.

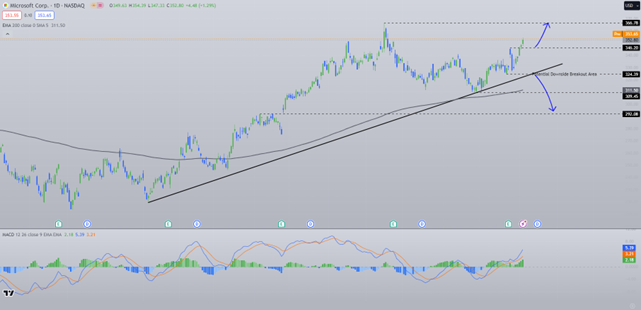

MSFT (EASYMARKETS: MSFUSD)

On October 24th, Microsoft Corp., together with other major US giants, delivered its earnings for Q3. EPS came out at 2.99 USD, against the estimated 2.65 USD, roughly a 12.66% rise. Revenue also grew, but at a slightly slower pace, rising by around 3.66%. However, the focus mainly fell on the company’s cloud and AI segments. Microsoft offers a cloud computing platform, which is called Microsoft Azure, or just Azure. This offers access, management, and the development of applications and services through global data centers. Sales of Azure rose by around 29%, and the company saw around 3% growth in AI-related services. cuts.

Lately, the world started looking at the top tech companies like Alphabet, Microsoft, Meta, and Amazon as if they are competing in a new game, which circles around cloud services and AI. Their original activities are getting pushed away due to the need for more innovation. To find something that makes the tech company stand out of the crowd is its ability to improve the part of its business relating to something that is currently receiving much hype. And at the moment, cloud services and AI are in the spotlight.

Microsoft is currently leading the way and very strongly promoting its AI side of the business, where Chat GPT is at the center of it. The AI search tool was created by Open AI, which Microsoft continues to pour money into. This is mainly done to develop the Chat GPT tool, which is believed to be integrated at a later stage into the Bing search engine. Currently, Chat GPT is available to the public free of charge. We believe it is a good tactic by Microsoft to compete with Google’s dominance. Google’s search engine is currently the go-to platform for any information. But once people get used to Chat GPT, it can take away, if not all, at least part of the market share from Google. Although Alphabet is currently working on its own version of the AI search tool, it is not yet even close to Chat GPT’s capabilities, hence why MSFT is now sitting as the top pick.

However, there are still threats to Microsoft and Open AI. If suddenly Chat GPT gets discredited and gets bad publicity for potentially being a biased search engine and only providing answers that could benefit a particular group. If something like this occurs, then other players like Alphabet, Meta, Amazon, or any other company that develops a similar product could have an opportunity to steal the throne.

AMZN (EASYMARKETS: AMZUSD)

On Thursday, October 26th, Amazon.com Inc. released its earnings report for Q3. Revenue saw around a 1.12% increase, whereas the EPS rose by a staggering 60.58%, going from the initial forecast of 0.58 USD to 0.94 USD. Although these readings are essential, everyone is focused on Amazon Web Services (AWS).

Amazon is currently pouring a lot of money into its AWS cloud business. This year, we saw AWS starting its own AI service, Bedrock AI, streamlining the development of large language models. Also, in September, Amazon invested 1.25 billion USD into a company called Anthropic, which is a direct competition to Microsoft’s Open AI. According to Amazon, they are expecting to quadruple their investment, but without any indication over what period of time.

So, the new measurement of the tech company’s performance is how well they are developing their cloud and AI services. And so far, Amazon could create some decent competition for Microsoft and Open AI. Well, at least that is how it looks like right now on paper. We will need more time to understand if Amazon can compete with Microsoft. In our opinion, AWS could choose to follow a different direction and enter another part of the industry, where it could implement and successfully use its AI services. This is not a bad tactic, allowing Microsoft and Alphabet to fight over who takes the reins of becoming the top search engine.

Regarding the AMZN stock, after a brief visit of the territory below the 200-day EMA on our daily chart, the price moved back up again. Certainly, such a reversal above the 200-day EMA is a positive sign, not to men-tion the breaking above one of its key resistance areas, which is between the 134 and 135 levels. This could potentially attract more buying interest in the near term. There could be more buyers jumping in if overall AMZN continues to trade somewhere above that trendline. At the time of writing, various analysts are set-ting their price targets, and it seems they are aiming for the area between the 160 and 177 levels.