What has happened so far

In the history of oil trading, April 2020 will be remembered as the day when WTI oil futures fell below zero, pushing deeply into negative territory. This moment was when fear ran quicker than logic and traders started selling oil, fearing that Covid-related lockdowns would slow the global economy to such an extent that oil demand would be equal to zero. Of course, this fear was an exaggerated idea, which we can distinguish by looking at the chart of WTI crude oil and the extreme dip we saw during April 2020. However, logic prevailed once again, and the price quickly started picking up pace, moving higher. By the end of the same year, the cost of the “black gold” rose back to just under the 50-dollar mark. 2021 was also a good year for oil and oil companies, as WTI gained around 50% by the end of that year, same as Brent.

The rally continued as we entered 2022. The strong move was mainly fueled by the start of the Russian-Ukrainian war and the sanctions imposed on Russia. Many analysts believed there would be a global oil shortage due to Russia’s inability to sell its oil to the usual buyers, such as the U.S. and Europe. Although the U.S. and the EU affirmed that they had stopped direct purchases of crude oil from Russia, this is not the case for indirect purchases.

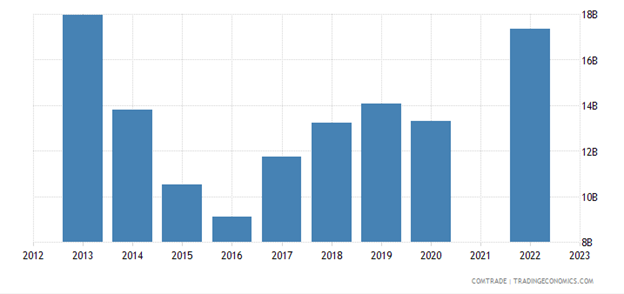

Some EU member states continue to purchase Russian oil, which is then supplied to Western Europe. One of the top current suppliers of crude oil to Europe is Kazakhstan. It is no secret that Kazakhstan has close ties with Russia. Kazakhstan continues to import oil and oil products from Russia and other goods and services. In fact, in 2022, the total number of Kazakhstan imports from Russia jumped dramatically, significantly surpassing the previous years.

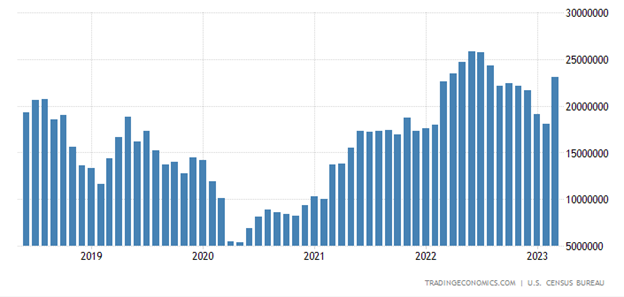

United States Imports of Total Energy-related Petroleum Products

As we know, India ramped up its Russian oil imports in 2022. During the first half of that year, the U.S. had increased its total imports of energy-related petroleum products worldwide.

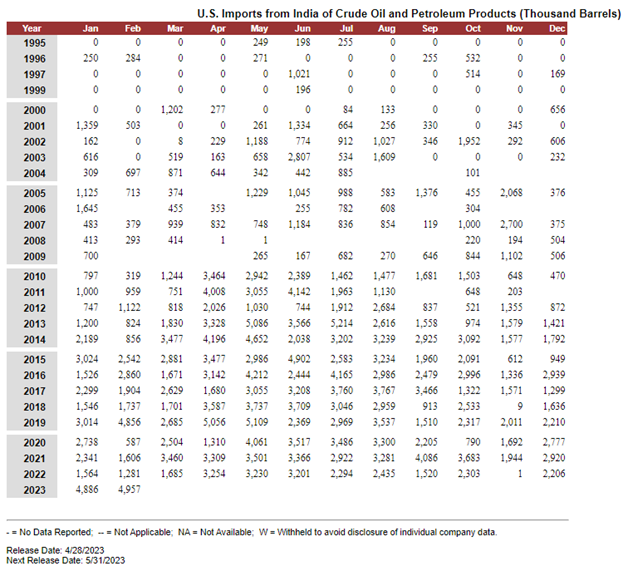

From the beginning of 2023, the U.S. started importing more crude oil and petroleum products from India. India is a country with a limited amount of oil reserves. In fact, it has proven reserves of only about 3 times its annual consumption. India is a major importer of Russian oil, so most of the U.S. imported oil from India could be of Russian origin. This means that we should trust the trade figures of major economies rather than official political statements.

So, this can explain why we have been seeing a decline in oil prices since the Russian-Ukrainian war broke out. Currently, there is no shortage of oil. The most recent comments of Saudi Arabia’s officials were that oil short sellers should be aware of possible oil production cuts, which may push the prices back up. However, shortly after, Russia’s Deputy Prime Minister came out with a statement, saying that Russia has no plans to cut oil production soon. This reluctance is understandable, as Russia heavily relies on its oil exports and revenues to continue running its economy.

Also, another reason for lower oil prices, in the long run, is that central banks of developed countries wish to keep their interest rates elevated as a method of battling inflation. Although we are currently seeing a slowdown in inflation, many central banks will stick to higher rates, at least in the medium term, to maintain inflation close to their targets. If that’s the case, higher rates may negatively impact economic growth, as it would be more expensive for businesses to borrow, especially the smaller ones. Such actions could hurt oil demand, making prices slightly lower overall.

Given all that has been mentioned above, nothing is certain. As we know, oil prices depend on our traditional demand/supply models and politics. The latter can easily influence short-term price shifts and disbalance the near-term outlooks.

The Technical View

Based on the technical picture of WTI crude oil on our weekly chart, we can see that from around the beginning of March 2022, the commodity has gradually declined. Around the beginning of September 2022, WTI broke and stayed below a long-term tentative upside support line drawn from the lowest point of April 2020. At the same time, the price is now trading below a couple of medium-term tentative downside lines, a steeper one taken from the highest point of June 2022 and a flatter one drawn from the highest point of February 2022. Although the medium-term trend is to the downside, the commodity has a strong floor, roughly between the 61.50 and 63.60 levels. A violation of that floor may attract more selling interest.

A break below the abovementioned support could invite more sellers into the game, possibly clearing the path towards the area just slightly above the psychological 50-dollar mark. We will aim for levels between 50.70 and 51.50, which mark the lowest point of June 2019 and February 2021, respectively. If that area cannot halt the slide, the next possible target might be around the 44-dollar mark.

Alternatively, if the previously mentioned steeper downside line gets broken, this may set the stage for a pushback to the current highest point of this year, at 83.50, which was tested in April. If that doesn’t slow down the bulls, the price could touch the other, flatter, tentative downside line drawn from the highest point of February 2022. Initially, WTI might stall there for a bit, but if that line eventually surrenders and breaks, this may signal a change in the direction of the medium-term trend. The next possible target then could be near 111 dollars. At several stages between the end of May 2022 and the beginning of July 2022, that area acted as a strong support hurdle and a resistance barrier.

Conclusion

Looking at the chart of WTI crude oil, it seems that the market is waiting for the next big catalyst to trigger either a huge sell-off or a big impulsive drive to the upside. Either way, the best solution right now is to wait for a breakout through one of our areas mentioned in the technical view above and also to continue monitoring the actions of the major central bank and its policies.

Additionally, the developments in the geopolitical arena should be considered, as those could be the initiators of short-term spikes of volatility in oil prices.